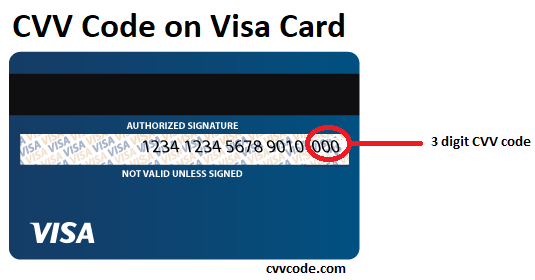

The three or four-digit number which you enter in the card verification value field during a purchase is called CVV Number. The acronym, CVV stands for “card verification code” and it verifies that the person making a credit card transaction is the legitimate owner of the card. The number is different from other numbers on a credit or debit card.

The CVV number is usually located on the back of the credit card, though newer cards may have it printed on the front or included as part of the magnetic strip. Some debit cards do not include a CVC number because transactions are processed without involving banks (which is why some online transactions can be performed using only an account number and a PIN).

A CVV code is an anti-fraud measure that prevents someone from using your card without your consent. The purpose of the number is to verify that you are in possession of the card. It does not guarantee that a transaction is legitimate, which means that it will not prevent unauthorized use of your card by a person with access to your physical card.

Your credit card number is a combination of digits and the CVV number is just one part of that larger set of numbers. The sequence you use during an online purchase tells the merchant that your credit or debit card is active and the person using it has possession of it. Without this, merchants would have no way to know whether you are an authorized purchaser or not.

This information is used during the authorization process where the credit card company verifies the number and authorizes a transaction for whatever amount you’ve indicated. This means that someone who has stolen your card number may be able to do some damage, but they won’t be able to access your funds unless they also have possession of the card itself.

The CVV code may be used during transactions where you are physically present at a point-of-sale terminal, such as in cases where you are using a debit or credit card for in-person purchase. Since this number can be relatively easy to guess for an experienced thief, it is not typically used in internet transactions.

Though information security can never be guaranteed 100%, there are many actions you can take to reduce your risk of having your cards compromised. Always make sure that your computer is protected by anti-virus software and a firewall. Make sure that you update these programs regularly, don’t open email attachments from people you don’t know and never click on links included in emails that seem suspicious.

You should also be careful when making purchases over the internet, particularly if you are buying something expensive or on a site, you’ve never used before. Unless guaranteed by PayPal, make sure to check the website for security signs like “HTTPS” at the beginning of the address, stay on the lookout for invoices that seem unusual or suspicious, and look for certificates issued by VeriSign or some other reputable third party.

If you notice anything suspicious, don’t do business with them and contact your credit card company to dispute any charges. Most importantly, only shop online at sites that use SSL encrypted connections. This ensures that the data you send is protected from prying eyes and cannot be intercepted by malicious users who may want to access your money for their own purposes.

However, changing card numbers is not always enough to prevent reputational harm. You should watch out for any signs of identity theft or fraudulent activity on your account because this could lead to problems when trying to open new accounts or otherwise verify your identity in the future.